“The stock market will do whatever it has to do to embarrass the greatest number of people to the greatest extent possible” – Walter Deemer

In our last letter, we found reasons to expect happier times for both stocks and bonds in 2023. In the first quarter, stocks and bonds were both positive by 7.5% and 3%, respectively.[1] On the surface, the results would indicate a calm recovery from a difficult 2022. However, the quarter was anything but calm. March was an especially dizzying month on the economic front with market narratives seemingly changing every week, summarized below:

- Entering the month of March, the narrative was for higher growth expectations and a more dire inflation outlook – all a product of stronger than expected economic data in February.[2] The result was the market pricing in more stubborn inflation and a Federal Reserve that still has work to do in cooling off the economy.

- The details in the February payroll release, during the second week of March, showed that the labor market was beginning to normalize. Hourly earnings continued to decelerate (deflationary).[3] Labor market conditions, especially hourly earnings, is a key focus of the Fed in their battle against inflation. The narrative changed to perhaps the economy can continue to grow with declining inflation in key areas.

- The big event in March was the run on Silicon Valley Bank (SVB), and concern around regional banks in general. This brought back scary memories of 2008, but the SVB event was not the same. 2008 was about leverage and bad assets on undercapitalized balance sheets. Today’s issue centers around liquidity around potential depositor outflows. Add in the arranged marriage between Credit Suisse and UBS with soft economic data and suddenly the market began pricing in a recession. In a clear sign that growth expectations were coming down, the US 2 Year Treasury rate peaked at 5.05% on March 8 and bottomed at 3.76% on March 23.[4]

Our bottom line is to not react to each economic datapoint. The market narrative will likely continue to oscillate between pricing in growth and recession. Our view continues to be that inflation is declining, with headline CPI at 5% in March since its peak at 9.1% in June.[5] We also believe the economy will continue to slow, possibly into recession at some point during the year. We also wouldn’t be surprised to see another “event” like SVB, as a result of an aggressive Fed in 2022.

With the continuously changing economic backdrop, the first quarter was feast or famine for stock returns. Across the S&P 500, the average stock was up 3.03% in the first quarter. That’s much lower than the 7.5% for the index, which means that the largest stocks gained more than the index.[6] A narrow market (a handful of big stocks carrying the index) can often mask mediocre returns for the rest of the market. There was also a complete change in market leadership from 2022.

Running completely opposite to 2022, the 10% of stocks in the S&P 500 with the highest valuations at the start of 2023 averaged a gain of 13% in the first quarter, while the 10% of the stocks with the lowest valuations averaged a decline of 2.5% in the quarter.[7] Some of this could be mean reversion with the market favoring the stocks that sold off the most in 2022. We could also see the market anticipating future lower interest rates, which generally favor higher valuation growth stocks. Right now, it’s too early to draw any meaningful conclusions. Regardless, it was a challenging first quarter with only 40% of active managers, as surveyed by Jefferies, beating their benchmarks.[8]

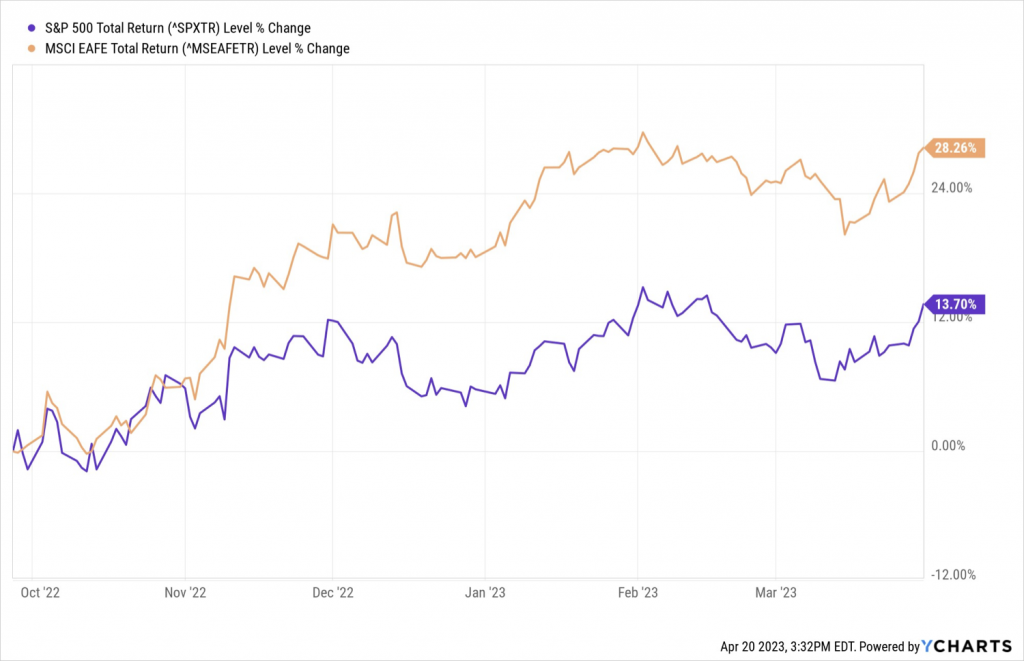

International stocks outperformed US stocks in the first quarter, continuing a trend we saw at the end of 2022. In our last letter, we noted that international stocks warrant our attention given the historical relationship between international stocks during periods of a weakening US Dollar (USD).[9] That relationship has held up since the USD’s decline of 10% since its peak on 9/27/2022, with the MSCI EAFE index outperforming the S&P 500 28.3% versus 13.7%.[10] Throughout the first quarter, we’ve added to international stocks while selling from commodities and US stocks. The decline in the USD along with Europe dodging a much-anticipated recession have quietly supported international stocks over the last two quarters.

To summarize our view on stocks, the narrow leadership within US equities is a bit of a caution flag telling us that perhaps things aren’t as good as the index is telling us. Right now, our work is telling us that international stocks present the best opportunity.

Finally, a comment on the financial world. If you consume financial media on a regular basis, you’d have good reason to think that the world constantly feels like it’s on fire. Many of these issues are serious and we must take them seriously as stewards of your wealth. However, perspective is important. Looking back on past challenges, we know that things often improve quicker than we think. The roller coaster never ends, the narratives will always change but we pride ourselves on being prepared, smart and calm in facing whatever markets throw our way.

As always, we’re here to answer any questions you may have.

Jack Piper

Founding Partner & Portfolio Manager

[1] Y-Charts 4/1/2023 Stocks S&P500, Bonds Barclays Aggregate Bond Index

[2] Natixis 4/1/2023

[3] Natixis 4/1/2023

[4] Y-Charts 4/1/2023

[5] Bespoke 4/14/2023

[6] Bespoke 3/31/2023

[7] Bespoke 3/31/2023

[8] Jefferies 4/2/2023

[9] Dorsey Wright 12/19/2022

[10] Y-Charts 4/20/2023