Market Updates • January 30, 2026

Market Update・2025 Q4 Review

Market Updates • January 30, 2026

“While uncertainty is never absent, discipline and perspective remain our anchors.”

We hope you had a peaceful holiday season and a nice start to 2026. The transition into the new year offers a natural moment to take stock of where we’ve been, recalibrate expectations and look ahead. Markets, like calendars, reset with fresh narratives and evolving opportunities. While uncertainty is never absent, discipline and perspective remain our anchors.

As we look ahead to 2026, markets continue to remain resilient in the face of a growing set of risks. While long-term investing remains grounded in discipline, process and diversification, we believe it is essential to be transparent about the key themes that could shape returns over the coming year. Here, we outline the themes we’re monitoring as we enter 2026.

First, let’s get the lay of the land

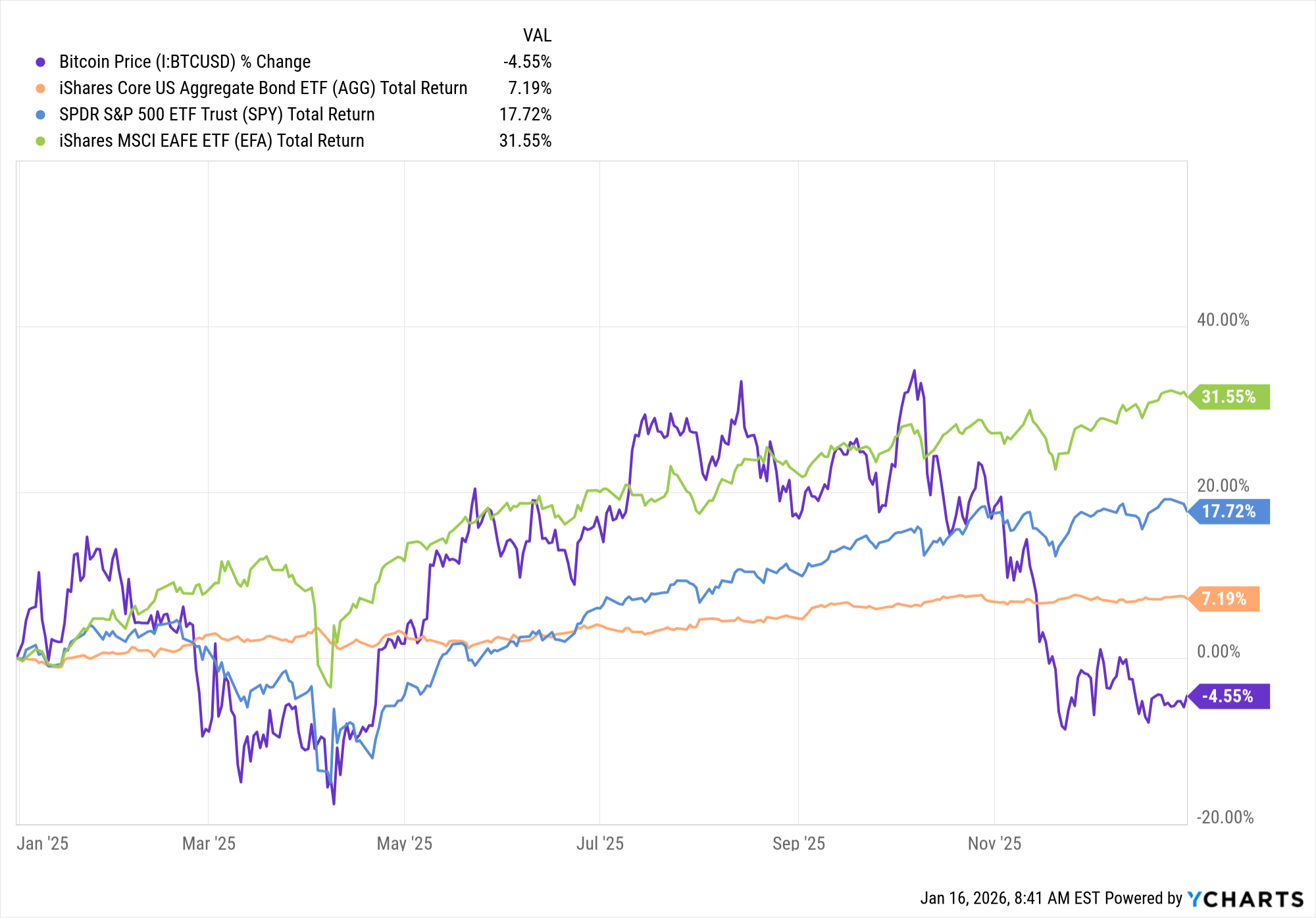

2025 started off tumultuously as concerns about protectionist policies and potential trade wars led to three consecutive months of losses for the S&P. The decline culminated in a four-day stretch that saw the S&P fall more than 12% after the announcement of reciprocal tariffs in early April. A week later, on April 9th, President Trump announced a 90-day pause on the tariffs, driving a 9.5% rally for the S&P, one of the index’s largest single-day gains since 2008 and among the 10 largest in its history.[1] With the administration eventually backtracking off their “Liberation Day” announcement, it was off to the races for the rest of the year as major asset classes, with the exception of Bitcoin, all posted solid gains for 2025.[2]

The current stock market setup shows Artificial Intelligence (AI) and semiconductor stocks driving market leadership. We’ve also seen a furious rally in precious metals, international stocks and a recent sector rotation into industrials, materials and financial stocks. With that backdrop, here is what we’re paying attention to in 2026:

Could this be the year of the 493?

As we’ve written about in the past, equity market performance in recent years has been driven by a relatively small number of large companies and themes (most often described as the Mag 7 – Apple, Microsoft, Google, Amazon, Nvidia, Meta and Tesla), particularly in areas tied to artificial intelligence and advanced technology.[3] While innovation remains a powerful long-term force, elevated valuations and a concentrated S&P 500 Index increase the risk of pullbacks in the index if expectations reset. At this point, the top 10 biggest stocks in the S&P 500 account for over 46% of the total market cap of the index.[4] For 2026, the key risk is not that these companies fail, but that their future growth is priced too optimistically and drag on the index.

Within US Equities, we’re seeing the market broaden from the Mag 7 stocks to the rest of the market without bringing down the S&P 500 Index. In our view, this is a positive development given that the top-heaviness of the index could create a scenario in which the market broadens but the index declines. As investors who believe in diversification across sectors, styles and geographies, this is something that we’ll continue to follow.

Signs of complacency?

Geopolitical tensions, shifting trade relationships, the rising US debt and political influence on free markets remain persistent risks in 2026. These forces can disrupt supply chains, pressure corporate margins, and increase market volatility with little warning. We’re also seeing a Federal Reserve whose independence is consistently and belligerently being threatened under the current administration.

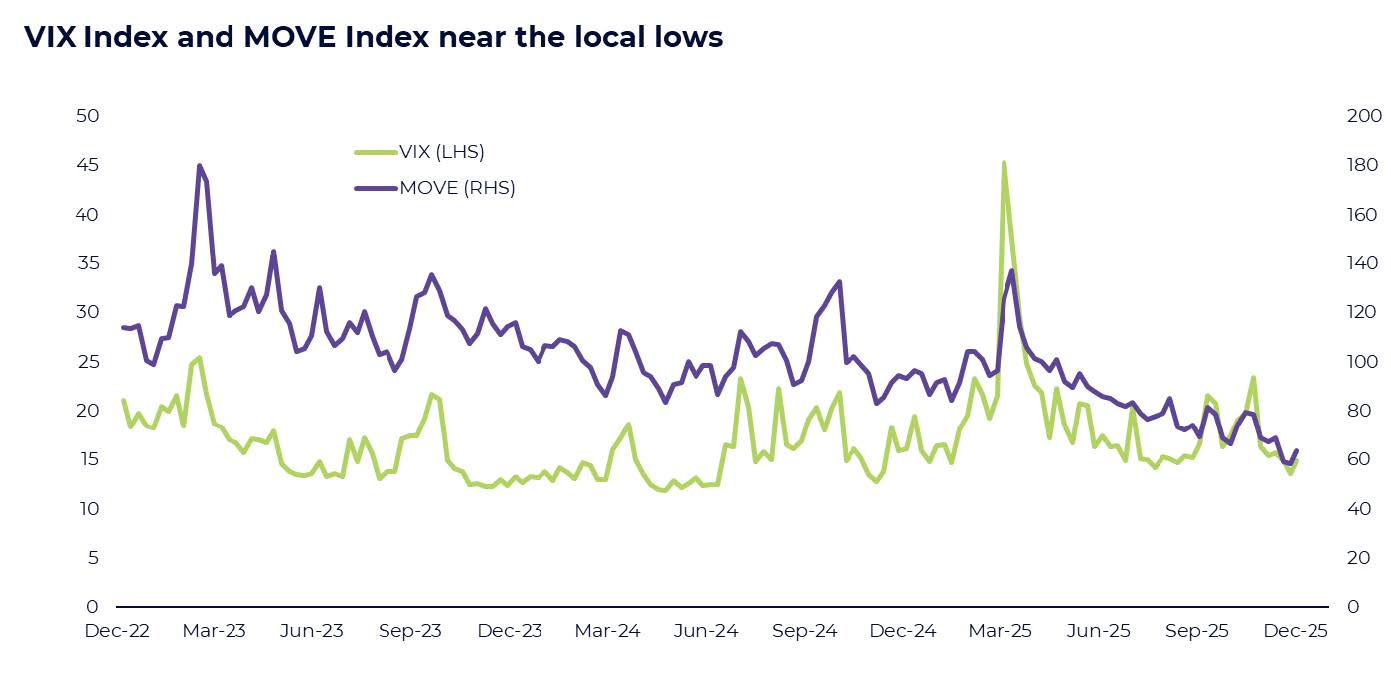

While markets generally consider armed conflicts and politics as just “noise,” however, it does leave some vulnerability to a volatility shock. Market measures of volatility (VIX for equities and MOVE for bonds) marched lower into the end of 2025.[5] That typically coincides with markets reaching all-time highs. While we don’t believe a material correction is in store, we think markets are underpricing volatility given the broader crosscurrents at hand and believe 2026 will see an increase in volatility. We continue to focus on global diversification, exposure to real assets, particularly precious metals and energy, where appropriate, and portfolio construction designed to withstand a wide range of economic and political outcomes.

Bullish on bonds

Given the economic backdrop we laid out in the third quarter of 2025, we expected the fourth quarter to be another good quarter in fixed income (bonds). This proved true, and we ended the year on a remarkable run for fixed income. Total returns in domestic bonds were the highest they’ve been in five years, having resembled what many would argue as being more of a long-term average equity performance.[6]

Whereas 2024 featured better bond returns on the shorter end of the maturity curve, 2025 brought interest rate cuts, along with market anticipation of further cuts with inflation fears subsiding, and the Fed shifting focus to slowing employment. The move in the interest rate curve accelerated returns on the shorter-term bonds while providing for a recovery in returns for longer-dated maturities. We ended the year with domestic short bonds returning 6.1%, intermediate bonds returning 7.0%, and long bonds 6.6%. Indeed, it was tough to find a weak spot in fixed income in 2025.[7]

How do we feel about bonds in 2026, even if overall yields are compressing? They are absolutely essential.

This holds especially true when considering the potential for a volatile upcoming year in equities. Great Diamond Partners believes in three equally important benefits of having fixed income in a diversified portfolio – a key mitigant to equity volatility, a consistent healthy generator of income and an efficient source of funding. In 2026, we believe fixed income will play a large role in all three aspects. With multiple years of significant equity returns, using fixed income instruments would be more tax efficient if there were a need for funding liquidity. The lack of perfect correlation to equities makes fixed income a good place to allocate towards with investors facing concerns geopolitically and economically. Finally, consistent income generation provides for a positive return push even if market prices decline after a multi-year run.

We maintain that the shorter end of the maturity curve is a good place to invest. Even if short-term rates fall further, the longer end may be stubborn and volatile. We cannot yet claim victory on inflation, with recent data showing consumer prices still too high for comfort. And while unemployment at 4.4% [8] is higher than where it’s been in prior years, that rise is modest and within full employment range (generally considered to be less than 5%). We see less of a need to lower rates to combat unemployment and slow job growth and more of a need to make sure a high-growth economic environment doesn’t accelerate too fast.

Our conclusion

While acknowledging that this doesn’t come without risk, we believe 2026 will be a positive year for both stocks and bonds. Despite the non-stop chaos in our news feed, the market is mostly focused on company earnings and interest rates. If earnings continue to grow, which we believe they will, and bond yields remain tame, 2026 is set for another good year for asset prices.

As always, we’d like to thank you, our clients, for your continued trust, partnership and support. We’re here to address any questions or concerns you may have. In the meantime, we wish you and your family a wonderful start to 2026.

[1] Dorsey Wright January 9, 2026

[2] YCharts January 16, 2026

[3] Magnificent Seven stocks are: Apple, Microsoft, Google, Amazon, Nvidia, Meta and Tesla

[4] Dynasty Financial Partners January 14, 2026

[5] Chart Source: Bloomberg December 2025

[6] YCharts, using weighted average Bbrg US Aggregate Index, Bbrg US High Yield Index, and Bbrg Municipals Index according to market size (AGG, USHY, TFI etfs as equivalents) 7.0% in 2025, 1.5% in 2024, 5.7% in 2023, -12.4% in 2022, -1.0% in 2021, and 7.3% in 2020

[7] YCharts January 16, 2026

[8] YCharts January 16, 2026

DISCLOSURES

Great Diamond Partners, LLC is an investment adviser in Portland, Maine. Great Diamond Partners, LLC is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Great Diamond Partners, LLC only transacts business in states in which it is properly registered or is excluded or exempted from registration. Great Diamond Partners, LLC’s current written disclosure brochure filed with the SEC which discusses among other things, Great Diamond Partners, LLC business practices, services, and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov.

This information should not be considered investment advice. Opinions expressed reflect the judgment of the authors and are current opinions as of the date appearing in this material only. While every effort has been made to verify the information contained herein, we make no representation as to its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All investing involves risk, including the loss of some or all of your investment.

Past performance does not predict future results.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular fund.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Specific investments described herein do not represent all investment decisions made by Great Diamond Partners, LLC. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

Hyperlinks in this piece are provided as a convenience, as we disclaim any responsibility for information, services or products found on websites linked hereto.

All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. There are no assurances that an investor’s portfolio will match or outperform any particular benchmark. Asset allocation and diversification do not ensure or guarantee better performance and cannot eliminate the risk of investment losses.

Market Update・2026 Q2 Review