Market Updates • April 25, 2025

Market Update・2025 Q1 Review

Market Updates • April 25, 2025

Every past market decline looks like an opportunity; every future decline looks like a risk.

MORGAN HOUSEL

Greetings from spring in Maine, where it’s snowing outside of my office in early April. We haven’t even had a “fake spring” day where we get 60 degrees and sunny. After living in the state for most of my life, you’d think that my expectations for April would’ve adjusted at this point. At least we know that warmer days are ahead.

As for markets, they’ve been caught in the middle of a terrible storm. After a strong finish to 2024, US equities faltered in the first quarter of 2025 as the S&P 500 finished down 4.3%, its worst start to a year since 2022. [1] Stocks had initially reacted positively to the results of the US presidential election, rallying throughout most of the fourth quarter and into the new year. However, worries about growth, stock valuations and the Trump administration’s tariff plans began to weigh on sentiment and stock prices. From its February peak, the S&P has now fallen more than 10%, putting the index in a technical correction. [2]

Are we done yet?

Let’s get a lay of the land here. As we wrote in our last quarterly letter, we were confident that there would be a 10% correction at some point this year. [3] Since 1928, the S&P 500 has averaged about one correction per year (1 every 346 days). [4] Note that there was no correction in 2024. As I write this, the S&P 500 is down 16% from its all-time high in February and it has come down with ferocity. [5] Anecdotally, this market decline is reminiscent of recent intra-year drawdowns like 2022 (-28%), 2020 (-35%) and 2018 (-20%).[6] This happens every few years, and the market has always recovered, usually quickly but sometimes slowly. Our opinion is that, barring a recession, this moment could be a good opportunity to buy stocks. Right now, the market is trying to figure out if the uncertain economic environment will tip us into a recession.

What’s going on with tariffs?

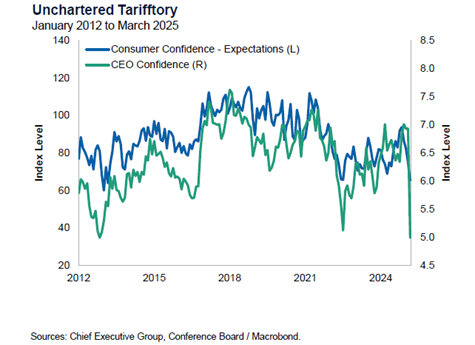

When President Trump was elected, we all expected some form of tariffs to be put into place, similar to what we saw in Trump presidency 1.0. Markets mostly gave the administration the benefit of the doubt until the Rose Garden announcement on April 2 when they were surprised by the size, scope, and methodology used. So, while the market was expecting tariffs in some form, clearly it had not discounted what was presented that afternoon. Whether the tariffs are being used as a negotiating tool, a revenue generator or a means to transform the entire global trade structure is anyone’s guess. What we do believe is that sustained high tariffs could disrupt supply chains, drive up prices and weigh on both businesses and consumers, ultimately dragging down economic growth. With already negative consumer and business sentiment, further restraining of spending is likely to show up in economic data.[7] In our view, the duration and intensity of tariffs will only exacerbate that phenomenon. Further, while corporate and household balance sheets were strong coming into this, the risks for recession have increased since the beginning of the year.

Is this all because of tariffs?

They’re part of the problem but not the sole culprit. The stock market setup coming into the year was an expensive and concentrated S&P 500 index. The forward P/E (price to earnings) ratio of the S&P 500 sat at 23.04x compared to its long-term average of 16x. This ranks in the 90th percentile since 1929.[8] We also came into the year with a very top-heavy S&P 500, with the seven largest companies representing approximately one third of the index.[9] This combination made the index vulnerable to an external shock.

Enter DeepSeek. The news of DeepSeek, a relatively unknown Chinese artificial intelligence (AI) company derailed the market momentum. Briefly, DeepSeek launched a new model that matched OpenAI’s performance on tasks like math, coding and reasoning for a fraction of the cost, making it a strong competitor.[10] This forced the market to question whether the incumbent AI leaders (many of The Magnificent Seven stocks) have invested far too much on AI and whether their lofty valuations were justified.[11]

The DeepSeek news kicked off a big unwind of the momentum stocks that had been carrying the index for several years. By the end of the quarter the combined Magnificent Seven stocks (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) were down 15.7%, while the overall S&P 500 was down only 4.3%.[12] The leaders in the index started falling before the tariff news really began in earnest.

Where do we go from here?

Whether fair or unfair, tariffs have stood out as the focal point for nearly all investor worries this year. All eyes will be on Washington, DC (or Palm Beach) for any clues on how tariffs evolve. The best way to describe markets right now is “twitchy” and we expect to see overreactions to any bit of clarifying news that comes out on the tariff front. Our biggest concern is that the longer tariffs are in place, the greater the chance of recession.

The good news is that asset allocation has been working. In the first quarter, bonds and international stocks were up 2% and 8%, respectively.[13] Diversification is carrying its weight, and we continue to make that an emphasis when managing portfolios.

To close, we thank you for your continued trust, partnership and support. As always, we’re here to answer any questions you may have. In the meantime, we wish you and your family a wonderful spring season.

[1] Dorsey Wright April 4, 2025

[2] Dorsey Wright April 4, 2025

[3] https://www.schwab.com/learn/story/market-correction-what-does-it-mean January 24, 2022. A “correction” is hen a stock index falls more than 10% from a recent high.

[4] Bespoke Investment Group December 21, 2024

[5] Y-Charts April 10, 2025

[6] Fidelity April 6, 2025

[7] Chief Executive Group, Conference Board / Macrobond April 3, 2025

[8] Bespoke Investment Group December 20, 2024

[9] Charles Schwab March 12, 2025

[10] Bespoke Investment Group January 21, 2025

[11] Magnificent Seven stocks are: Apple, Microsoft, Google, Amazon, Nvidia, Meta and Tesla

[12] Y- Charts April 10, 2025

[13] Y-Charts April 11, 2025 bonds represented by the AGG ETF and international stocks represented by the EFA ETF

DISCLOSURES

Great Diamond Partners, LLC is an investment adviser in Portland, Maine. Great Diamond Partners, LLC is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Great Diamond Partners, LLC only transacts business in states in which it is properly registered or is excluded or exempted from registration. Great Diamond Partners, LLC’s current written disclosure brochure filed with the SEC which discusses among other things, Great Diamond Partners, LLC business practices, services, and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov.

This information should not be considered investment advice. Opinions expressed reflect the judgment of the authors and are current opinions as of the date appearing in this material only. While every effort has been made to verify the information contained herein, we make no representation as to its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All investing involves risk, including the loss of some or all of your investment.

Past performance does not predict future results.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular fund.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Hyperlinks are provided as a convenience, and we disclaim any responsibility for information, services or products found on websites linked hereto.

Specific investments described herein do not represent all investment decisions made by Great Diamond Partners, LLC. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

Market Update・2025 Q4 Review