Market Updates • January 23, 2025

Market Update・2024 Q4 Review

Market Updates • January 23, 2025

It’s tough to make predictions, especially about the future.

YOGI BERRA

We hope you enjoyed a relaxing holiday season and New Year. As we kick off 2025, we’re at the time of year where everyone is making predictions on what the next twelve months will hold. Our industry is no exception, with market strategists at big banks assigning their year-end price targets for the S&P 500. While it’s always fun to make an educated guess, usually these targets become moving targets as the year evolves and the investment landscape changes. We won’t try to predict the ultimate finishing point for the market this year, but we will dust off our crystal ball on what we think will drive markets and the economy for 2025.

2024 Year-in-Review

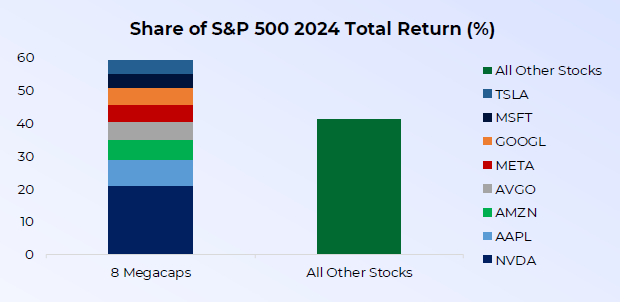

We’ll start with a brief review of 2024, which was another banner year for the American stock market, as the S&P 500 rose by 25%. This comes on the heels of the S&P 500 rising by over 26% in 2023.[1] Similar to 2023, 2024’s returns were primarily driven by companies leading and/or benefiting from the artificial intelligence (AI) arms race. The “Magnificent 7” tech giants, plus Broadcom, accounted for 60% of the S&P 500 returns in 2024.[2]

Economically, inflation moderated across the globe with most central banks entering rate-cutting mode.[3] The US economy also saw five quarters in a row of real GDP growth averaging +3% year over year, solidly above the average of the past 15 years of +2.4% year over year.[4] In our opinion, lower inflation, above trend growth, combined with low unemployment provided a powerful tailwind for stocks. However, as we know, Wall Street is not Main Street, and voters made it clear in the voting booth that prices are still too high.

November’s election saw 80% of incumbents voted out, and populist movements gaining traction, culminating in Donald Trump winning the presidency.[5] Following the election, there was an immediate boost to investor sentiment and stocks rallied on the optimism that lower taxes, a lighter regulatory environment and more efficient government would offset any negative impacts of new policies towards trade and inflation.[6] As of this writing, the euphoric rally in stocks following the election has mostly reversed as, in our view, investors need clarity on the economic policies of the second Trump administration.

That all brings us to the present. Below are three things to pay attention to in 2025:

The Fed began an easing cycle at their September meeting and has cut rates by a full percentage point since then. During the same period, 10-year Treasury yields have risen by about 1% – an unusual occurrence and one that demands close attention.[7] In our opinion, the reason behind this could be concern over fiscal imbalances, deficits and/or a policy misstep from The Fed if they overestimate their progress on inflation and underestimate the strength of the economy. Admittedly, it’s still not entirely clear at this point. Regardless of the reason, we believe that a yield at or above 5% could cause some problems for stocks. Why yields are on the rise matters, though. If they’re rising because of stronger growth, that should be positive for stocks. If they’re rising due to higher inflation expectations, that would be a negative. Separately, this presents a nice opportunity for bond investors to lock in more attractive yields. We’ll be paying close attention to the treasury market and what it’s trying to tell us.

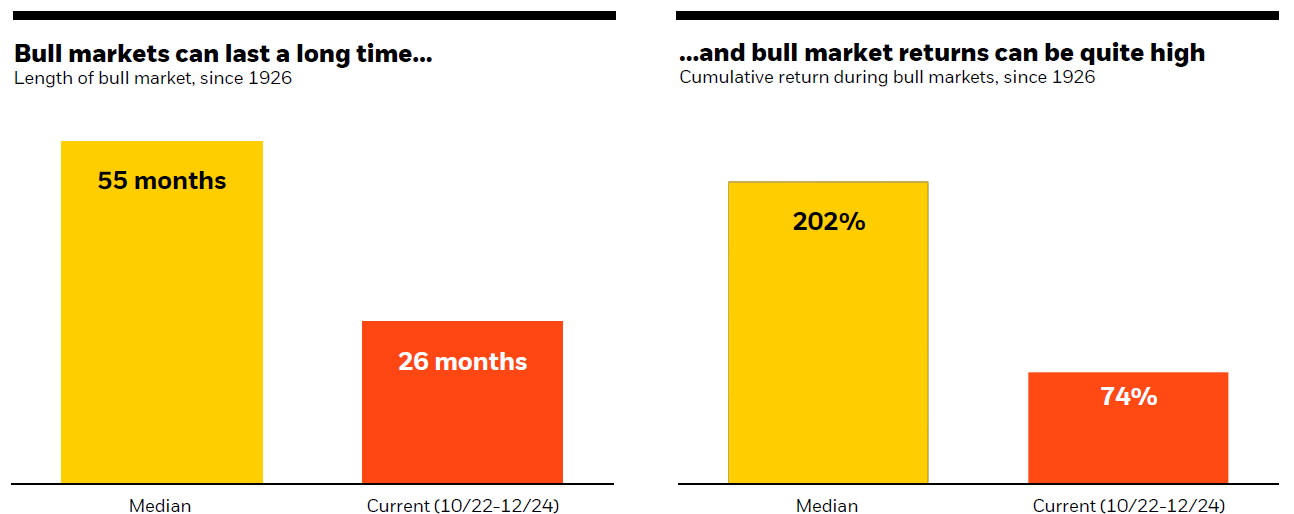

When a stock index falls more than 10% from a recent high, it is often said to have entered “correction” territory.[8] Since 1928, the S&P 500 has averaged about one 10%+ correction per year (1 every 346 days). 2024 didn’t see a 10%+ correction and 2021 was the last year (other than 2024) to not see one.[9] Today, and as we’ve written about a lot over the past few years, the S&P 500 index remains top-heavy, with the Magnificent 7 stocks accounting for 33% of total market capitalization.[10] This can be a double-edged sword. While the Magnificent 7 stocks have lifted the broader market over the past two years, a downturn in these stocks could drag the index down even if the remaining 493 stocks are strong. In addition, in the chart above from Goldman Sachs, the market-cap weighted S&P 500 (where the Magnificent 7 equal 33% of the index) is considerably more expensive on a forward price to earnings basis than the equally-weighted version of the index.[11] Our takeaway is that 1) the broader market is vulnerable to a correction, which would be completely normal even if it doesn’t feel like it at the time and 2) a diversified portfolio with flexibility remains critical to risk management.

The bottom line

Our bottom line is that we expect moderate equity returns this year as economic growth and valuations (especially for mega-caps) normalize. The US economy should remain resilient, supported by fiscal momentum and innovation in key sectors like AI and energy transformation. Market volatility, geopolitical tensions and fiscal and economic policy missteps must be monitored.

As always, we’d like to thank you, our clients, for your continued trust, partnership and support. We’re here to address any questions or concerns you may have. In the meantime, we wish you and your family a wonderful start to 2025.

[1] Y-Charts January 4, 2025

[2] Chart source: Dynasty Financial Partners January 13, 2025. Magnificent 7 stocks are: Apple, Microsoft, Google, Amazon, Nvidia, Meta and Tesla

[3] Dynasty Financial Partners January 13, 2025

[4] Natixis January 15, 2025

[5] Dynasty Financial Partners January 13, 2025

[6] Bespoke Investment Group December 28, 2024.

[7] Dynasty Financial Partners January 13, 2025

[8] https://www.schwab.com/learn/story/market-correction-what-does-it-mean January 24, 2022

[9] Bespoke Investment Group December 21, 2024

[10] Bespoke Investment Group December 28, 2024

[11] Chart source: Goldman Sachs January 13, 2025

[12] JP Morgan Asset Management January 1, 2025

[13] Natixis January 15, 2025

[14] Chart source: Morningstar and BlackRock as of 12/23/24. Stock market represented by the S&P 500 Index from 3/4/57 to 12/31/24 and IA SBBI U.S. Large Cap TR Index from 1/1/26 to 3/4/57. This illustration assumes reinvestment of dividends and capital gains January 14, 2025

DISCLOSURES

Great Diamond Partners, LLC is an investment adviser in Portland, Maine. Great Diamond Partners, LLC is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Great Diamond Partners, LLC only transacts business in states in which it is properly registered or is excluded or exempted from registration. Great Diamond Partners, LLC’s current written disclosure brochure filed with the SEC which discusses among other things, Great Diamond Partners, LLC business practices, services, and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov.

This information should not be considered investment advice. Opinions expressed reflect the judgment of the authors and are current opinions as of the date appearing in this material only. While every effort has been made to verify the information contained herein, we make no representation as to its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All investing involves risk, including the loss of some or all of your investment.

Past performance does not predict future results.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular fund.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Hyperlinks are provided as a convenience, and we disclaim any responsibility for information, services or products found on websites linked hereto.

Specific investments described herein do not represent all investment decisions made by Great Diamond Partners, LLC. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

Market Update・2025 Q2 Review