Market Updates • October 30, 2025

Market Update・2025 Q3 Review

Market Updates • October 30, 2025

“In the world of investing, we too go through seasons … Each has its own distinct role.”

We hope you had a wonderful summer. As the days grow shorter and the air turns crisp, we’re reminded that the seasons never fail in their rhythm. Autumn, with its golden hue and cooling winds, is more than a change in temperature—it’s nature’s reminder that transition is both inevitable and essential.

In the world of investing, we too go through seasons. There are times of rapid growth, like spring; periods of abundance, like summer; moments of rebalancing, like autumn; and occasional hibernation or retreat, like winter. Each has its own distinct role.

The third quarter is now in the rearview. While it has historically been the weakest quarter of the year, the S&P 500 ended up +8.1% for the quarter to push its year-to-date gain above 14%.[1] After a summer of expansion (and dare we say some complacency) we’re seeing pockets of volatility and a reorientation of expectations. Historically high valuations, rising capital spend in technology companies, and echoes of past bubbles are leading some investors to question where we are in this current bull market. We’ll address that and a few other topics below.

Are we in an AI bubble?

If you consume financial news you’re likely aware of the Artificial Intelligence (AI) boom and the parallels to the technology bubble of the late 1990s. History has shown that bubbles are often driven by exuberance around an asset class, attracting capital and new investors. Typically, a bubble will exhibit rapidly rising asset prices and extreme valuations, often driven by an increased use of leverage.[2] The challenge in real-time is that bubbles are irrational and impossible to predict.

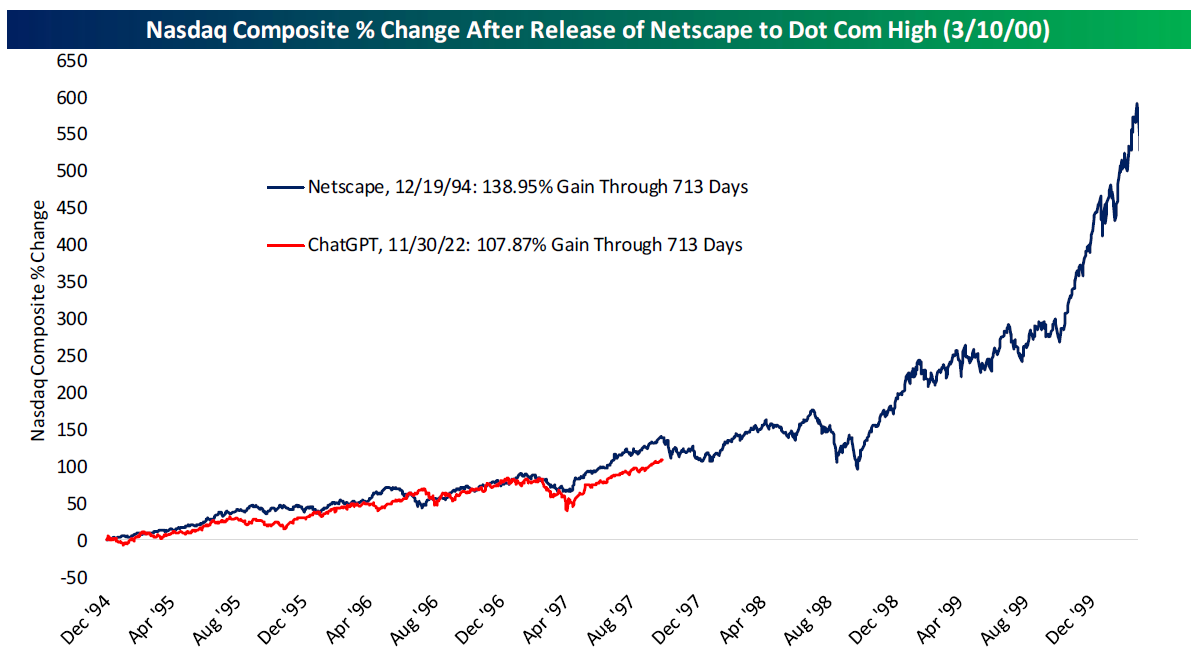

Today’s market continues to be driven by the performance of companies engrained in or adjacent to AI. This bull market began in the month before the release of ChatGPT in November of 2022 and it hasn’t stopped since. ChatGPT, which sparked the age of AI, is now seen as on par with the release of the web browser Netscape Navigator back in 1994, the dawn of the internet age. The chart below has been making the rounds of late.[3] When comparing the performance of the Nasdaq since Netscape’s release to its performance since ChatGPT was released, the results are eerily similar.

While we don’t make investment decisions based on a single chart, if this analog holds, we’re only in the middle of the AI Boom.

Fundamentally, we see differences between past bubbles and the current AI investment environment.

That doesn’t mean we haven’t been paying attention. Over the course of the year and especially last quarter, we’ve taken the opportunity to trim back some of our AI exposure that has grown beyond the target allocation and reallocated to other parts of the market. This is not us expressing any sort of view on when the AI momentum will end. Rather, it’s our job to properly manage risk in portfolios. As certain positions get too big, we need to manage that.

The bond market seems to be OK with elevated uncertainty

Heading into the last quarter of the year we expect the Federal Reserve (Fed) to cut two more times (there are two more meetings in 2025) and then likely pause to take inventory of its effects in 2026. The path of least resistance is still lower for rates in 2026. Consensus today believes two to three additional cuts, according to probabilities implied by 30-day Fed Funds futures prices at the Chicago Mercantile Exchange (CME), as the Fed wants to get back to neutral (~3.0%) from its previously restrictive stance.[6] Lower short-term interest rates typically mean better bond prices (more demand as investors push to lock in fixed coupons ahead of falling market rates). Assuming the economy continues to avoid recessionary pressures on balance, we expect fixed income to be favorable again for clients in Q4.

At this point in time the bond market isn’t showing any concern about an imminent recession.[7] While US economic policy uncertainty remains historically elevated, credit spreads aren’t signaling any kind of stress.[8] Corporate fundamentals remain solid, supported by a favorable economic backdrop and healthy balance sheets with manageable leverage. While pockets of stress exist within credit markets, overall conditions remain stable. Despite elevated policy uncertainty under the current administration, rate volatility has stayed contained – providing a firm foundation for corporate bond spreads to remain tight. The catch is that spreads can only go so low and right now there isn’t much room for error if growth quickly slows and bonds need to be repriced.

While this anticipated positive total return in fixed income is welcome, Great Diamond Partners puts more emphasis on three pillars of fixed income ownership benefits above performance: overall portfolio volatility offsets, correlation diversification, and client liquidity needs. We believe fixed income can provide consistent income generation while lessening the burden of market swings on performance in a more tax-efficient manner, as well as offering potential returns that do not perfectly correlate to those of stocks at any given time. We remain positioned on the shorter end of the rate curve, where history tells us marginal risk-adjusted returns are more pronounced inside of seven years in any rate environment.

Bottom line

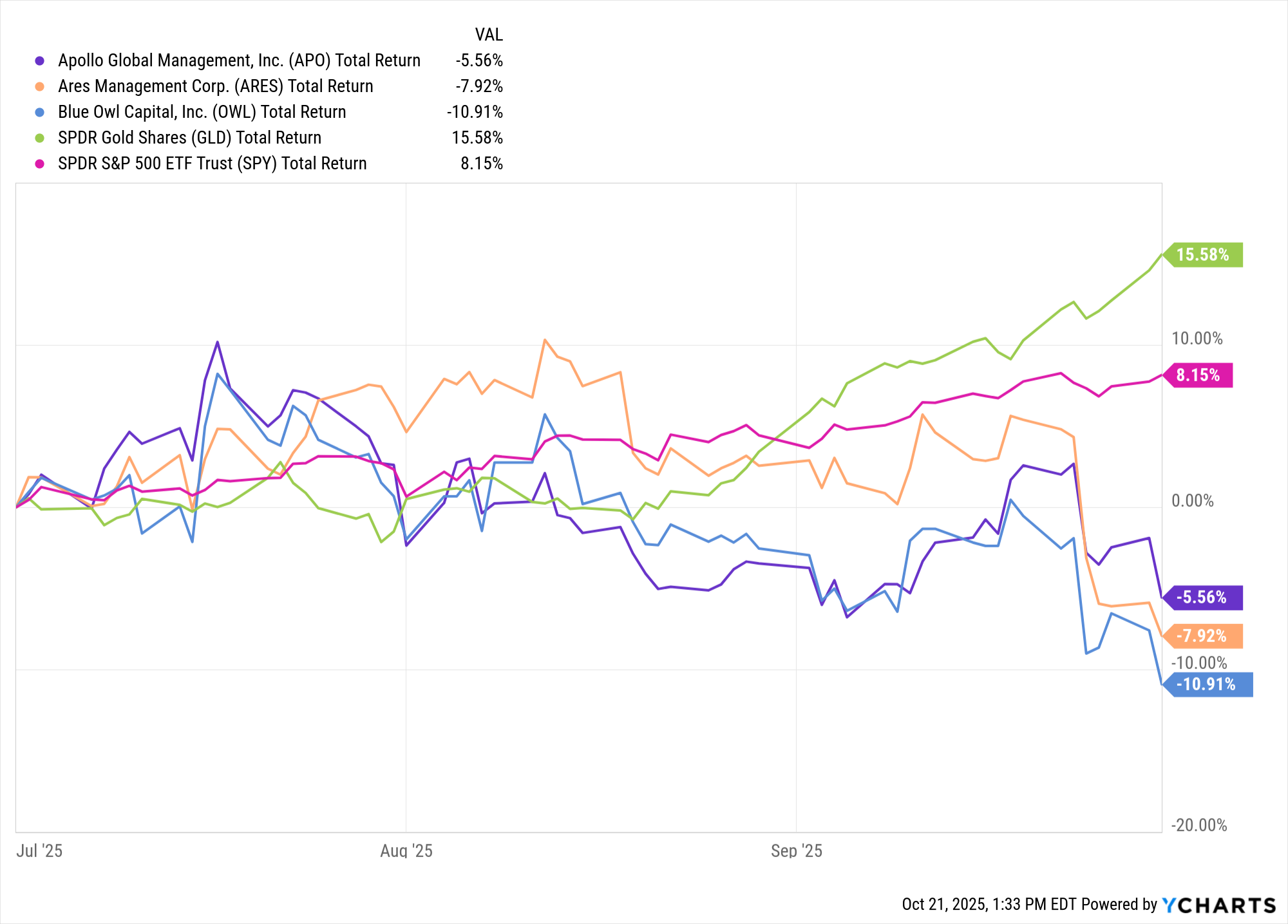

The weight of the evidence remains positive, and we remain bullish on the market and economy into year-end while acknowledging that we live in a world where things could go wrong in short order. The Wall of Worry of market narratives continues to be recycled[9]: valuations and bubbles, market concentration, complacency and uncertainty around economic policy. The bottom line for us remains simple: corporate earnings continue to grow in a slowing (but not yet slow) economy, and that’s what matters to the market.[10] While there’s validity to the recycled narratives, we’re also focused on what the surge in gold and the weakness in stock prices that serve as proxies for private credit are telling us.[11] Our philosophy – price leads fundamentals in the market and economy – tells us that these price movements can’t be ignored.

As we close we’d like to thank you, our clients, for your continued trust, partnership, and support. As always, we’re here to answer any questions you may have. In the meantime we wish you and your family a relaxing and peaceful holiday season.

[1] The Bespoke Report, October 3, 2025

[2] Goldman Sachs. October 8, 2025

[3] The Bespoke Report, October 3, 2025 (Chart Source)

[4] Goldman Sachs, October 8, 2025

[5] Fidelity, October 13, 2025

[6] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html October 20, 2025

[7] Y-Charts, October 20, 2025. Data is from a source believed to be reliable but not guaranteed

[8] The Bespoke Report, October 3, 2025. Credit spread definition: The spread between high yield and investment grade corporate bonds and comparable Treasuries that measures how much extra compensation investors demand for taking on credit risk

[9] Investopedia, https://www.investopedia.com/terms/w/wallofworry.asp. Wall of Worry description: Wall of worry is the financial markets’ periodic tendency to surmount a host of negative factors and keep ascending. Wall of worry is generally used in connection with the stock markets, referring to their resilience when running into a temporary stumbling block, rather than a permanent impediment to a market advance.

[10] Natixis, September 18, 2025

[11] Y- Charts, October 21, 2025. Data is from a source believed to be reliable but not guaranteed

DISCLOSURES

Great Diamond Partners, LLC is an investment adviser in Portland, Maine. Great Diamond Partners, LLC is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Great Diamond Partners, LLC only transacts business in states in which it is properly registered or is excluded or exempted from registration. Great Diamond Partners, LLC’s current written disclosure brochure filed with the SEC which discusses among other things, Great Diamond Partners, LLC business practices, services, and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov.

This information should not be considered investment advice. Opinions expressed reflect the judgment of the authors and are current opinions as of the date appearing in this material only. While every effort has been made to verify the information contained herein, we make no representation as to its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All investing involves risk, including the loss of some or all of your investment.

Past performance does not predict future results.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular fund.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Specific investments described herein do not represent all investment decisions made by Great Diamond Partners, LLC. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

Hyperlinks in this piece are provided as a convenience, as we disclaim any responsibility for information, services or products found on websites linked hereto.

All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. There are no assurances that an investor’s portfolio will match or outperform any particular benchmark. Asset allocation and diversification do not ensure or guarantee better performance and cannot eliminate the risk of investment losses.

Market Update・2025 Q4 Review