Market Updates • July 30, 2025

Market Update・2025 Q2 Review

Market Updates • July 30, 2025

“When we construct client portfolios, we build them to prepare for any outcome, not any single outcome.”

We hope you’re having a relaxing summer. Summer has hit its stride in my family, as we had the chance to take a much-anticipated trip to California to visit friends. From the spectacular beauty of the Carmel coastline to the quiet calm of Sonoma County, it was a refreshing pause filled with quality time, good food, perspective, and a lot of rental car miles. It reminded me of the importance of long-term thinking, planning and the value of endurance through ever-changing landscapes – concepts that very much apply to our investment philosophy.

Long-term thinking certainly applied in the second quarter. While finishing the quarter a bit higher than 10%, the S&P 500 experienced what can only be described as a multi-day crash in early April following President Trump’s “Liberation Day” tariff announcement, plunging over 10% in only a few trading days (and almost 20% from its all-time high in February).[1] Sure enough, the market got through to the administration and, on April 9th, a 90-day tariff pause was announced.[2] Since then, we’ve been impressed with the Wall of Worry that the market has continued to climb: multiple geopolitical concerns, trade uncertainty, a less accommodative Federal Reserve and a budget battle set to expand the fiscal deficit. Yet, here we are at all-time highs.

Where do we go next?

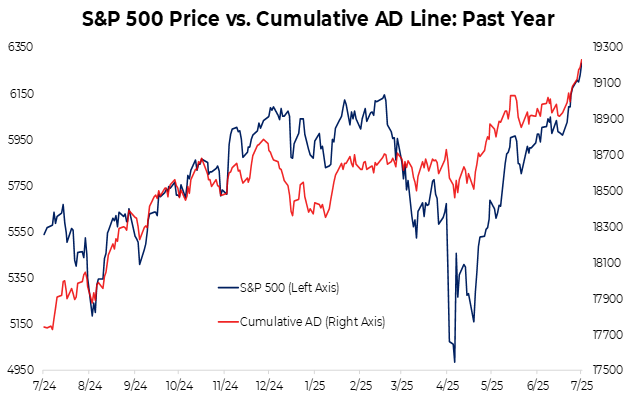

After seeing a bit of everything in the second quarter, what do we expect to see for the second half of the year? A few things are catching our eye when it comes to stocks. First, after years of market concentration (that we’ve written about like a broken record), the broader market is finally participating. Driven by Financial, Industrial and Consumer Discretionary stocks, more stocks have participated in the recent market gains as shown through a positive Advance Decline (AD) Line.[3]

Breadth, as measured by the S&P 500’s AD Line, and price, now sit at all-time highs. We feel this kind of broadening is a positive sign and suggests that a more balanced and sustainable move higher is possible for stocks in the second half of the year. In our view, the backdrop of more resilient economic data, modest inflation and solid earnings growth validates the most recent move in stocks.

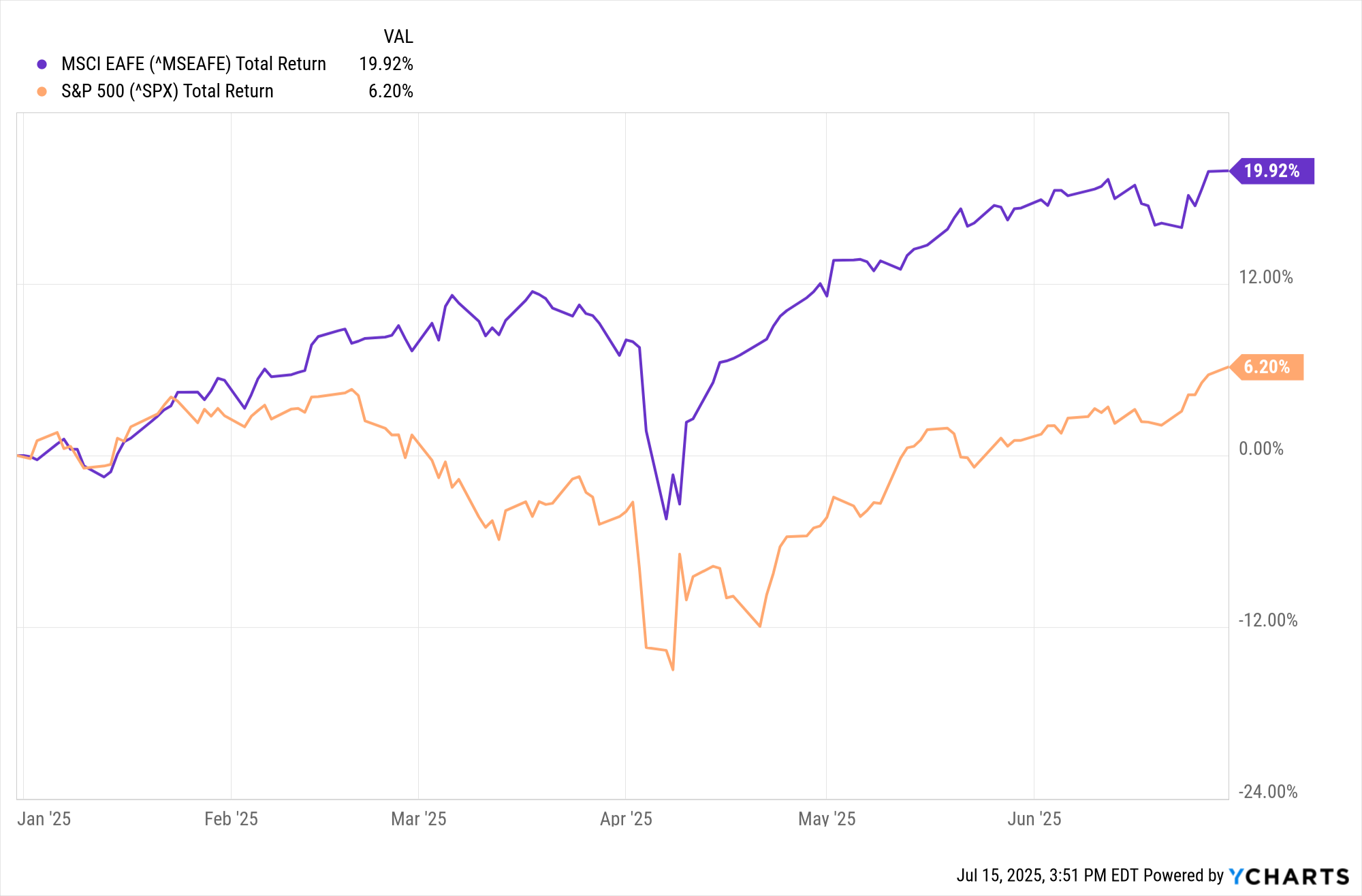

Second, we’re continuing to stick with our allocation to international equities. While our stock market had a nice bounce back in the second quarter, the US has had its weakest performance versus the rest of the world in the first half of the year since 2002.[4]

We think that while international equities outperformed in the first half of the year, it’s not time to move away from regional diversification.[5] A weaker US Dollar, coupled with policy uncertainty in the US and cheaper valuations abroad should provide a strong case that diversification into international equities is well-warranted at this point.

The role of bonds

The extreme fear seen in the markets during those April days was reminiscent of past market crises with peak uncertainty and signs of capitulation in the stock market. When we construct client portfolios, we build them to prepare for any outcome, not any single outcome. The good news: a well-diversified portfolio does that for you. This doesn’t mean you won’t feel the whiplash watching the market move around. But you can rest easier knowing you don’t have to bet your future on one scenario or the other. Bonds play a big role in building a portfolio prepared for any outcome.

Starting with high inflation and a Federal Reserve aggressively hiking rates in 2022, it has been tough sledding for bonds over the last few years. For clients who own bonds, we continue to advocate for exposure to address liquidity needs, portfolio volatility offsets and diversification. This past April was a real-life case study for the role of bonds in a portfolio. In the first six trading days of April, the S&P 500 quickly dropped 11.5%. In stark contrast, US bonds in aggregate were down just 1.3%, with US Treasuries down just 0.5% and investment grade corporate bonds, which tend to correlate more to stocks, down 2.5%.[6] The ability to sustain wealth can be just as powerful as creating wealth.

A note on the tax bill

After a marathon session Congress passed the Trump Administration’s tax and domestic policy bill, and President Trump signed it into law on July 4. The law includes extended and expanded tax cuts, including a permanent increase in the lifetime gift and estate exemptions, increases to the state and local tax deduction (SALT) and standard deduction, among others.[7]

We’ll have more information in the coming weeks and months about how the new law may affect your financial plan. In the meantime, please reach out with any questions about the legislation or anything else that’s on your mind.

An update from the investment team

We’d like to welcome Mark Doehla to our investments team. Mark joined us in May, and we couldn’t be happier to have him on board. As we’re always striving to improve, Mark will be working to enhance our investment offerings. I know he looks forward to meeting you.

To close, we thank you for your continued trust, partnership and support. As always, we’re here to answer any questions you may have. In the meantime, we wish you and your family a relaxing and peaceful remainder of the summer.

[1] Y-Charts July 14, 2025

[2] Bespoke, April 9, 2025

[3] Chart Source: Dynasty Financial Partners, Bespoke Investment Group, Bloomberg July 13, 2025

[4] Bespoke, June 27, 2025

[5] Y-Charts July 15, 2025

[6] Y-Charts July 21, 2025. US Aggregate bonds represented by AGG ETF, US Treasuries represented by GOVT ETF, Investment Grade Corporate bonds represented by USIG ETF.

[7] Verrill Dana LLP, July 16, 2025

DISCLOSURES

Great Diamond Partners, LLC is an investment adviser in Portland, Maine. Great Diamond Partners, LLC is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Great Diamond Partners, LLC only transacts business in states in which it is properly registered or is excluded or exempted from registration. Great Diamond Partners, LLC’s current written disclosure brochure filed with the SEC which discusses among other things, Great Diamond Partners, LLC business practices, services, and fees, is available through the SEC’s website at: www.adviserinfo.sec.gov.

This information should not be considered investment advice. Opinions expressed reflect the judgment of the authors and are current opinions as of the date appearing in this material only. While every effort has been made to verify the information contained herein, we make no representation as to its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All investing involves risk, including the loss of some or all of your investment.

Past performance does not predict future results.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular fund.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Specific investments described herein do not represent all investment decisions made by Great Diamond Partners, LLC. The reader should not assume that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

Hyperlinks in this piece are provided as a convenience, as we disclaim any responsibility for information, services or products found on websites linked hereto.

All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. There are no assurances that an investor’s portfolio will match or outperform any particular benchmark. Asset allocation and diversification do not ensure or guarantee better performance and cannot eliminate the risk of investment losses.

Market Update・2025 Q4 Review