“Hope smiles from the threshold of the year to come, whispering ‘it will be happier’…” Alfred Lord Tennyson.

With 2022 in the books, investors are looking forward to a new year, hoping for a happier outcome. The abridged recap for 2022 is that stocks, as measured by the S&P500, had their worst year since 2008, down over 18%[i]. Bonds had a historically bad year with the Bloomberg US Aggregate Bond Index down over 13%, the worst year since the inception of the index[ii]. The breakdown of the typically complimentary relationship between stocks and bonds made 2022 one of the most challenging investment years in recent memory. As the calendar year changes, the market issues of 2022 haven’t gone away: there’s still a war, unacceptably high inflation and a hawkish Federal Reserve (The Fed). However, we’re starting to see reasons that make us hopeful for a happier 2023.

Inflation and Federal Reserve

The Fed remains squarely focused on inflation by embarking on the most aggressive rate-hike cycle since the early 1980s. If someone told you that a year ago, you’d laugh. Last December, Fed officials were in good agreement that the Fed Funds rate would be right around 1% by the end of 2022. In reality, we finished the year with a Fed Funds rate just under 4.5%[iii]. The result was financial markets constantly trying to catch up with the Fed in terms of interest rate pricing. This game of uncertainty and catchup rippled through all asset classes. It appears that, after nine months, markets have caught up with the Fed. The result has been a reduction in volatility within stock, bond and currency markets.

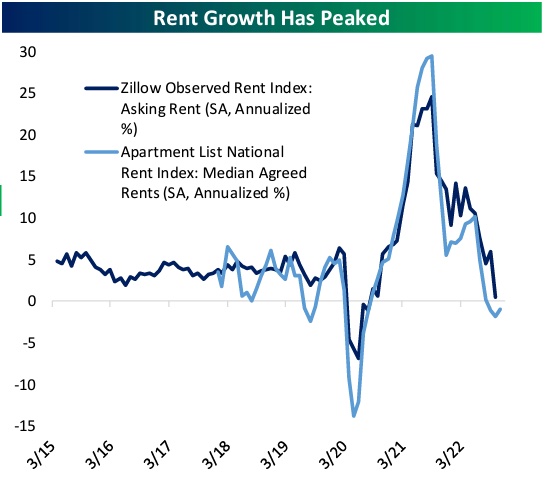

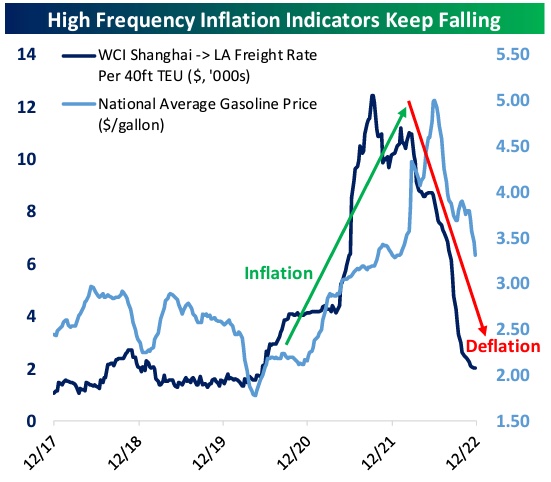

Looking at inflation components, the backdrop has become much more positive. Very broadly, shipping rates have been falling since late 2021, national average gas prices are heading back down to $3.25 a gallon from their peak of $5 and rent growth has peaked. We feel comfortable saying that inflation peaked over the summer.

(Source, Bespoke (12/23/2022)

The most important outcome from the last year? In our opinion, The Fed is close to the finish line in this hiking cycle. We believe there is less uncertainty for the future path of rate hikes and a deceleration in inflation, both of which are good for risk appetite.

Markets

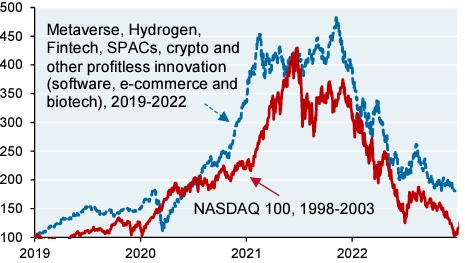

The unanticipated surge in rates last year resulted in lower valuations for stocks and, as 2023 begins, we see stock valuations back to pre-Covid levels. While we can’t argue that stocks are cheap, the excesses seen in the 2020-21 markets have been wiped out, and the forward price to earnings multiple of the S&P 500 is back to its recent historical average. The damage in stocks was especially acute in the profitless companies and the cryptocurrency landscape – resembling the bursting of the Tech Bubble over 20 years ago. Fortunately, we invested in quality (i.e., profitable) companies and were spared of the worst damage. As we did in 2022, we continue to favor value stocks instead of growth.

(Source, Bloomberg, JPMAM, 12/27/2022)

The question for 2023 is how will the monetary tightening of 2022 impact the economy and, therefore, corporate earnings? Recession concerns are legitimate and the consensus for corporate earnings growth this year is no growth at all[i]. While that doesn’t sound good, it’s important to know that new bull markets typically begin several months before near-term earnings estimates are revised downward[ii]. The market, as it always does, will begin putting more weight on a recovering 2024 outlook rather than today. 2023 could very well be a better year for stocks than the overall economy.

Sticking with stocks, the most notable change we’ve made in many portfolios has been increasing exposure to international equities. Sampling the last 10 years, US stocks have significantly outperformed international stocks[iii]. However, in the fourth quarter of 2023, developed market international stocks gained 17% compared to just over 7% for US[iv]. There are a few reasons for this outperformance but the biggest reason, we believe, is the weakening of the US dollar during the fourth quarter. A combination of geopolitical risks and an aggressive Federal Reserve led to significant appreciation in the dollar. As inflation began to soften, so did the dollar, declining by 8% in the fourth quarter[v]. Since 1985, international equities, on average, have outperformed US stocks during periods of a weakening dollar[vi]. With the US dollar in a downtrend, we believe international stocks warrant our attention.

For bonds, starting points matter. Higher interest rates and higher yields make the start of 2023 a much more attractive environment for bond investors compared to a year ago. With inflation having peaked, the bond market has stabilized and bonds will go back to playing their more traditional role in portfolios. A shock in inflation could change that but, as we’ve mentioned, we believe inflation trends are in our favor.

Bottom Line

While hope isn’t an investment strategy, there’s evidence to make us think that 2023 could be a happier year for investors. Inflation has moderated, stock valuations have come down to acceptable levels and volatility in bond and currency markets have subsided. Inflation remains too high and we’re not out of the woods, but the data tells us we’re on the right course. As we pointed out in last quarter’s letter, since 1926 and following peak inflation rates, average returns for stocks and bonds are positive for the next 12 month period.[vii] There are whispers of happier times ahead.

We wish you and your family health and prosperity in this new year. We’re grateful for your continued trust in us. Please don’t hesitate to reach out to us with any questions or concerns.

Jack Piper

Founding Partner & Portfolio Manager

[i] Y-charts 12/31/2022

[ii]Dorsey Wright 1/6/2023

[iii] Bespoke 12/23/20222

[i] Goldman Sachs, 1/6/2023

[ii] Calamos, 1/3/2023

[iii] Y-Charts SPY v EFA 12/31/2012 – 12/31/2022

[iv] Dorsey Wright 1/6/2023

[v] Dorsey Wright 1/6/2023

[vi] Dorsey Wright 12/19/2022. Downtrend is defined as a decline of 10% or more from peak. Comparing EFA v SPY

[vii] Blackrock 9/30/2022

Disclaimer:

Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional adviser should be consulted before implementing any of the strategies or options presented. Past performance doesn’t guarantee future results.

It is possible to experience loss with an investment including your principal investment.

The S&P500 is made up of 500 large corporations. It is not possible to invest directly in an index.

The Bloomberg Aggregate Bond Index is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.